5 minutes to understand Hybrid Stablecoins with Frax V1

N.B.: This article is for an audience that already have knowledge of cryptocurrencies. The V1 protocol is now outdated but allows to understand the concepts behind the FRAX protocol. The V2 version will be the subject of a future article.

Stablecoins are cryptocurrencies indexed to a fiat currency like the dollar or assets like gold. They are an important source of innovation in the cryptocurrency ecosystem and particularly in the DeFi ecosystem. We will see how Frax stands out from the existing protocols and how its V1 works.

1/ The stablecoin protocols today

Currently, there are three main families of stablecoin protocols:

Centralized collateralized protocols

A trusted third party ensures that the total amount of stablecoins in circulation matches the total amount of the fiat currency reserve. Projects such as Tether’s USDT or Circle’s USDC are some examples. The main risk in these projects is the “Custody Risk” since the projects have control over the reserve funds. Moreover, the intermediation model is contradictory to decentralization, the ideological and economic principle of blockchain.

Over-collateralized decentralized protocols

A decentralized protocol issues a stablecoin in proportion to a pool composed of several stable or volatile cryptocurrencies. The collateral ratio is higher than 100% in order to reduce the risk of liquidation if the value of the crypto-currencies in the pool decreases. One example is the DAI. These models ensure a high level of decentralization but lose economic efficiency by over-collateralizing the reserve.

Algorithmic protocols

They are not based on collateral but on algorithmic processes that are supposed to stabilize the currency. Some examples are Basis or Empty Set Dollar. These models are “trustless” and economically efficient but not functional in practice. No algorithmic stablecoin has yet succeeded in providing short or long term price stability.

2/ Frax, a hybrid model

Frax is a hybrid model that falls somewhere between the algorithmic and the collateralized model.

The objectives are to provide:

- Economic efficiency through under-collateralization

- A trustless model without “Custodial Risk”

- High scalability

- A decentralized protocol governance

This protocol is composed of a collateral ratio of x% and an algorithmic rate of 1-x%. The protocol is 100% collateralized at launch, then the algorithmic share increases as the level of confidence in the protocol improves.

It is composed of two tokens: FRAX, which is the stablecoin indexed to the dollar, and FXS, which is the protocol’s utility token and is volatile. The collateral pool is composed of several stablecoins such as the USDC. The protocol will accept later volatile cryptocurrencies as collateral.

Thus, for each FRAX in circulation, there is a collateralized rate in USDC (to simplify, we consider USDC as the only collateral) and an algorithmic rate in FXS.

To create FRAX, the user sends a certain amount of USDC and a certain amount of FXS defined by the collateral ratio. The FXS sent are “burned”, i.e. removed from the quantity in circulation.

To withdraw FRAX from circulation, the user sends FRAX on the protocol and receives in exchange a certain amount of USDC from the reserve and a certain amount of minted FXS, i.e. created and added to the circulation.

3/ Price stabilization mechanisms

The stability of the price at its “peg” is based on simple arbitrage mechanisms. The following diagrams help to understand the stabilization mechanisms when the FRAX price varies.

The price of FRAX increases:

(The diagram is available HERE for the mobile versions.)

The FRAX price decreases:

(The diagram is available HERE for the mobile versions.)

4/ The FRAX Market Cap and the FXS deflationary mechanism

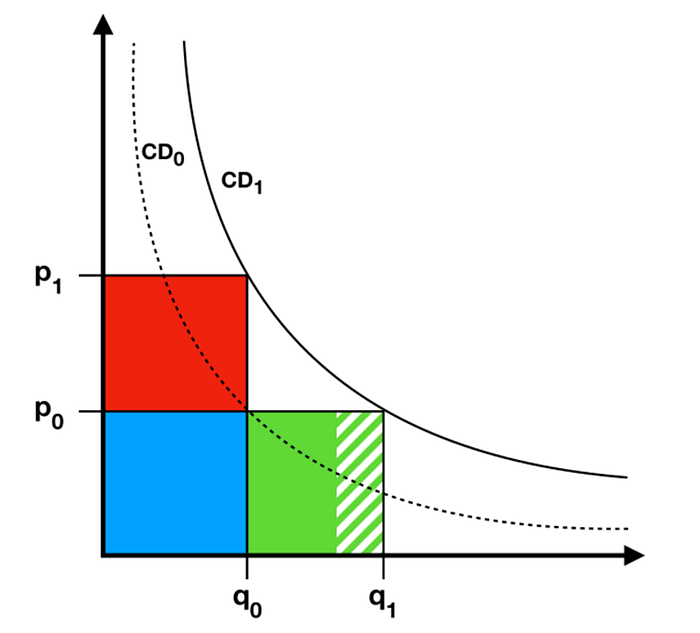

We can infer from the previous diagrams that the Market Cap of FRAX varies with that of its price. The following diagram allows us to better visualize the link between stabilization mechanisms and Market Cap:

We assume an initial equilibrium (p0;q0) that is p0=1$ and q0=100 with the blue area representing the total Market Cap.

If the FRAX price increases, we have p1=1,1$. There is therefore an imbalance situation, FRAX are then minted by the arbitrageurs. (diagram 2)

We therefore have an increase in the quantity of FRAX and a decrease in the price, i.e. a new equilibrium (p0;q1) with the blue and green areas representing the total Market Cap.

It is interesting to note that the hatched area represents the quantity of FXS burned to reach the new equilibrium. So as the Market Cap of FRAX increases, the amount of FXS in circulation decreases. The FXS therefore follows a deflationary mechanism, which makes it relevant in terms of “Tokenomics”.

5/ The collateral ratio

The tokens that can be exchanged during the “mint” or “redeem” process depend on the collateral ratio. For example, with a rate of 80%:

If a user mints the token then he has to send $80 of USDC and $20 of FXS to get 100 FRAX. The 20$ of FXS are burned so only 80$ goes into the reserve. We have 100 FRAX created for $80, which is a 80% collateral.

If a user redeems the token then he sends 100 FRAX and gets back 80$ of USDC and 20$ of FXS minted. We have 100 FRAX burned for 80$ USDC in the reserve so a 80% collateral.

In the V1.0 version:

The collateral ratio moves at the inverse of the FRAX Market Cap. When the Market Cap is increasing, the collateral ratio decreases by 0.25% per hour and vice versa. For example, if the collateral is 50% and the FRAX Market Cap is increasing for 3 hours, then the collateral ratio will be 49.25%. Thus, the protocol considers that an increase of the Market Cap is a sign of confidence so the algorithmic rate can grow.

In the V1.1 version:

The collateral ratio depends on the evolution of the Market Cap of FRAX and the total quantity in $ of FXS used in Liquidity Providing on DEX :

Gr = S(FXS) / S(FRAX)

with Gr = Growth ratio,

S(FXS) = Total supply in $ of FXS in LP,

S(FRAX) = Total supply in $ of FRAX

If the price of FXS increases → the Market Cap increases → S(FXS) increases → the slippage on DEX decreases

Since we have an increasing Market Cap and decreasing slippage, we can then increase the share of FXS in the collateral ratio without fearing effects on FXS volatility.

Conversely, if the price of FXS decreases, the share of FXS in the collateral ratio decreases, so fewer FXS are burned or minted, which tends to decrease its volatility.

Buyback and recollateralization

If the collateral ratio changes, then there is an imbalance in the reserve between the expected and the actual amount of collateral. Again, an arbitrage mechanism allows to return to equilibrium:

(The diagram is available HERE for the mobile versions.)

Conclusion

The hybrid mechanism of FRAX is relevant because it allows to introduce an increasing algorithmic part as the resilience of the protocol grows.

The V2 version introduces the concept of an “Algorithmic Market Operations Controller”. It allows price stabilization, collateral ratio variation and market operations in various DeFi protocols.

(The V2 version will be the subject of a future article)

Disclaimer: None of the content in this article is an investment advice. The author of the article has no partnership with the projects presented.